This week I’m stepping beyond media headlines and sharing my personal experience with Sydney’s property market across various budgets and buyer types, with an educated guess on where we’re heading for the next few months.

Our upsizer buyers $1.5m-$6m are seeking more bang for buck and are becoming less compromising on their wish-lists. A negative sentiment driven by the Iran scenario + rate rises in March was exacerbated by a large release of listings post Easter hols in April.

Many didn’t sell and were withdrawn, and auction clearances tanked.

Sydney property prices for the past three months are down .9%. By my reckoning the $2m-$6m sector is down probably 4%-8% with the official numbers offset by a buoyant first home buyer segment. I am now seeing first signs of vendors declining to sell into a softer market with City fringe/East/Inner West Torrens title listings down around 18% from a fortnight ago. We may see a return to the 2023/2024 season where fewer listings propped up prices despite rate rises, or prices may drift a little lower if owners decide this market is the new normal and they’re happy to sell and buy in the same market.

The Sydney investor market is slow. Key lenders have advised all loan approvals will be assessed according to the legislated budget changes which is causing uncertainty. For opportunistic buyers there is the option to finance with 2nd tier lenders or private debt- not bound by APRA servicing regs. The investors we see still active are SMSF buyers and seeing small builders/family consortiums bidding up solid duplex and value add sites.

Our downsizer cash buyers and well positioned and still active, being less concerned with rate rises and pleasantly surprised as homes that may have been out of budget as late as last November are now sliding back into range. Sydney seller/buyers are operating in the same market however we recently had the pleasure to assist a downsizer sell out of a hotter Newcastle market and buy into a more moderate Inner West Sydney market.

That opportunity doesn’t come up often.

The first home buyer market up to $1.5m is robust. Our first home buyers are informed, focused and risk averse- reluctant to push to the upper end of their limits. They often have a plan to buy more modestly, add value and/or reduce debt then convert that to an investment when they take the next step in 2-5 years.

Here are two properties we’ve purchased for first home buyers in recent weeks. The brief was the same for both and reflects the mandate for many market entrants; prove the case for strong capital growth , and a decent and improving rental yield in a high demand area.

$1.48m purchase- 3 bed 2 bath 2 car 125sqm on title. 11% pa capital growth forecast 5.1% gross yield in yr 1. Purchased off-market.

$850k purchase- 3 bed 1 bath 1 car 110sqm on title 5 mins walk from new metro station. 11% pa capital growth forecast 5.5% gross yield in yr 1. Purchased off-market.

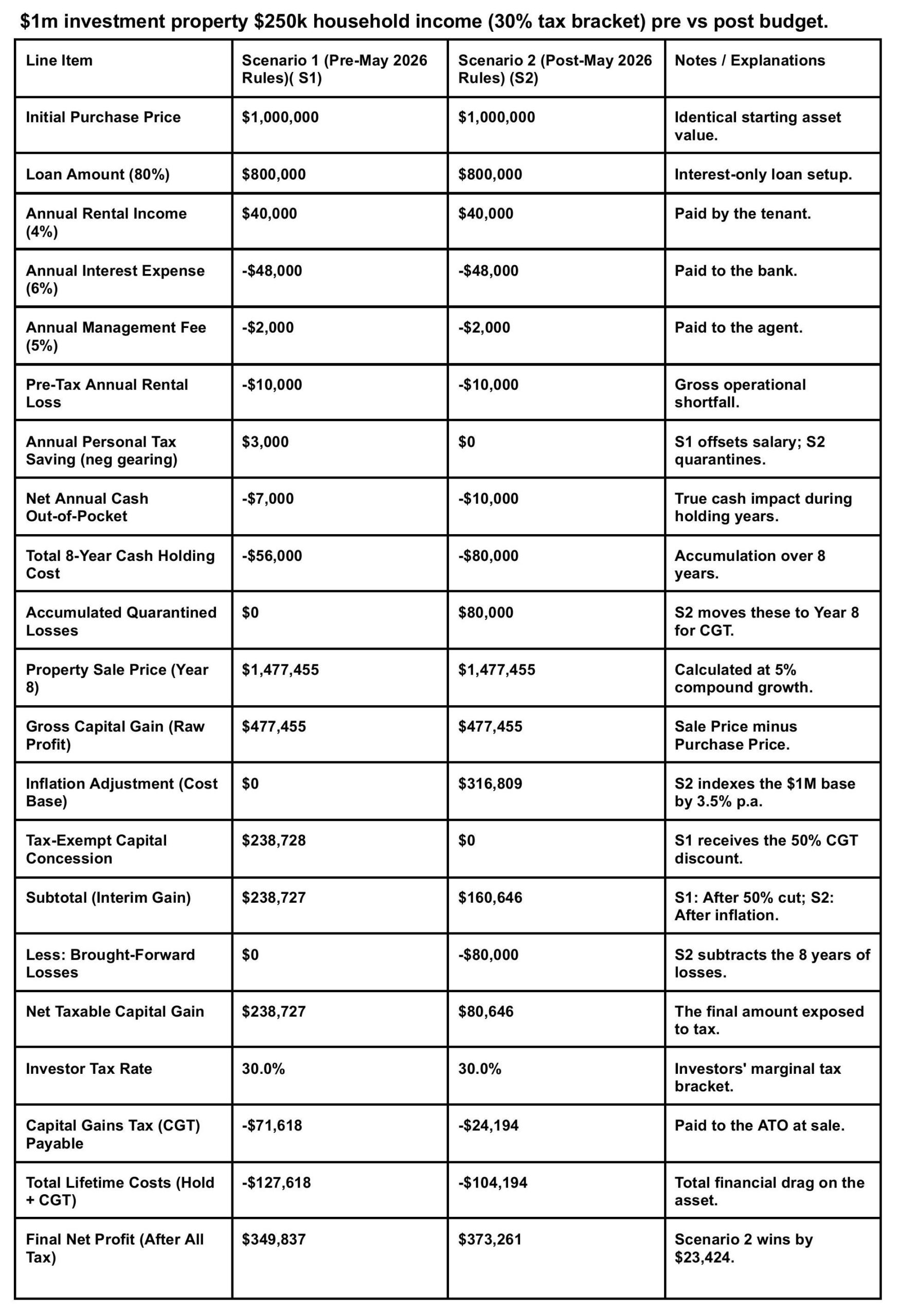

New budget settings – bad for investors?

On a final note, I was over hearing claims that buying existing property will no longer stack up for investors. We don’t buy new/off plan so i ran some numbers:

My modeling shows existing property still stacks up, in some circumstances better than under the old model. When inflation runs higher and capital growth is moderate then the new budget settings can actually work better for investors than negative gearing and 50% cgt concession- thanks to indexation and the ability to offset carried losses at full dollar value.

In a low inflation (and probably lower interest rate) high capital growth environment investors still win.

Surely it’s only a matter of time for investors to cotton on and return to accumulate existing build properties. For the financial planners and accountants reading this i’d love to hear your thoughts on this one.

That’s all for now. Any q’s comments or criticisms – please get in touch.