As a buyers agent I have the privilege of experiencing property market action at the ‘coal face’.

Every day I speak with sellers and buyers across Sydney for apartments, terraces, houses.

A common approach many are taking since interest rates increased and property prices softened has been to ‘wait and see’ what happens.

Potential sellers wait and see because they’re fearful of not achieving a good price. Our psychological and financial well-being is closely tied to our property wealth and we go to great lengths to avoid selling and losing out.

This is why the level of stock on-market is at five year lows and why good properties are scarce.

Potential buyers are waiting and seeing too.

Many have FOOP- fear of over paying, and believe rising interest rates and falling prices will result in better affordability, more properties to choose from, and perhaps even a chance at a bargain via a distressed sale.

But many of these assumptions are just that. Let’s take a closer look.

Does the property market have further to fall?

Maybe.

The Australian property market is cyclical- there are periods of increases, disproportionally larger than the following periods of decreases.

The current down market is our fourth since 2007 with peak to trough falls of -9% -7% and -10% during the last three downturns with the current downturn at -6% as of December 2022 and likely closer to -9% at the time of writing (March 2023) Note these are national averages.

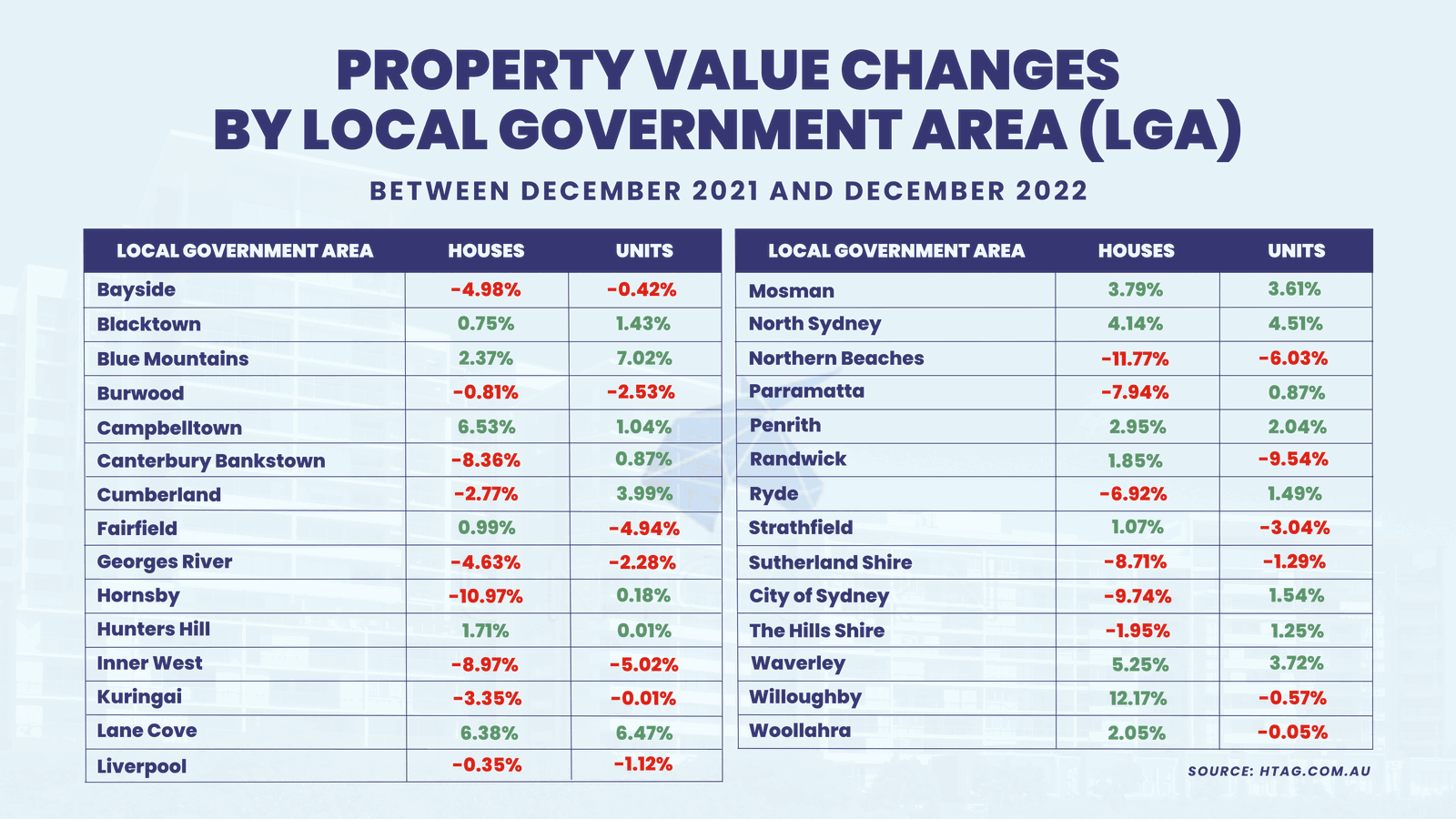

Price movements between Sydney LGA’s (local government areas) and the different types of housing stock within them have each performed quite differently to the national average and to each other. My experience buying in many of these LGA’s throughout 2022 and into this year reflects the statistics. Waverley, Mosman and Lane Cove have remained more challenging to buy in, especially for property with a land component, whilst units in Randwick have noticeably softened.

Bondi and the Inner East have stabilised, Redfern and Marrickville still feel like they may drift a touch lower.

The biggest downside risk isn’t the anticipated interest rate rises, which are already priced in- it’s the impending ‘mortgage cliff’.

Over the balance of 2023 31% of outstanding mortgage debt rolls from fixed to variable rates.

The average loan size is $539,000 with those homeowners moving from around 2% to a 5.5% interest rate, paying an extra $1100 a month.

The numbers appear worse for mortgagees in blue chip Sydney suburbs with loans typically twice that amount or more, although income and ability to repay are higher.

Corelogic has an interesting perspective on the mortgage cliff and you can read about that here. Eliza Owen also concludes that many households will feel the pinch, in particular owners with one or more negatively geared investment properties where even the recent big rent hikes may not be enough to cover the increased holding costs.

Based on old data for those rolling from fixed to variable rates from September 2022 we can see loan defaults have not materially increased, nor have distressed sales. They may materialise. Many argue it is against the interests of our government to allow mass defaults or a material decrease in the property values that banking institutions hold as assets on their balance sheets. There are already predictions of intervention scenarios such as the mortgage repayment holidays we saw in 2020.

Yes, the market may well fall further. So let’s consider the effect of a peak to trough price fall of 15% in an affluent suburb.

A Bondi apartment that was $1.5M at the peak could then be yours for $1.275M if you were able to time your purchase at the market bottom.

However during that same period we would have endured a dozen interest rate rises, with the offical rate going from .1% to a forecast 4%

As a rule of thumb your borrowing capacity decreases by 10% for every 1% of interest rate rises so you can now borrow 40% less.

In May 2022 with standing pre approval, a $300k deposit and a $200k income you could have borrowed the $1.3M required for your $1.5M Bondi apartment.

In May 2023 your max borrowing will be $780K allowing you a maximum purchase of only $1.08M.

This reduced affordability comes as a shock to most. Falling property prices caused by rising interest rates don’t put more and better homes within our grasp, they push them further beyond our reach.

To make matters worse the property market functions on speculation. Confidence returns on the rumour of a rate decrease and prices will move away further before your affordability improves or you jump back into the market and find something you’d like to buy.

Property prices increase over time because upswings are larger and faster than downturns. In the table below you can see previous one to two year downturns have seen 7-10% price falls and two to three year upswings have seen 30-40% increases. These increases in absolute dollar terms mean saving a bigger deposit, or scoring a pay rise aren’t enough to keep your buying power on par with rising prices.

So what’s the solution?

I suggest that If you already have a fully assessed pre approval, now is definitely a good time to buy.

If you have a deposit and secure employment, then now is a good time to speak to a broker about your borrowing capacity and ready yourself to buy.

Don’t dwell on the past or wait for the future. Recalibrate your strategy to buy the best quality you can afford within your means today.

Competition is lower with fewer committed buyers and more realistic sellers.

Off-market property opportunities are increasing as market conditions encourage sellers to trade quickly and quietly.

Hire a professional to find you the properties others don’t see, and to play the inside game to buy at the sharpest price.

Take advantage of this rare window of opportunity where you have more negotiating power.

The wait and see approach when it comes to property has historically not achieved great outcomes.

Taking action today is a much clearer path to a great result.